Authored by SNHU Vice President of Student Experience Innovation Timothy Lehmann, Assistant Vice President of Financial Literacy & Integrity Misty Sabouneh, and CHEPP Director of Policy and Advocacy Brittany Matthews

Three years ago, on March 13, 2020, the federal government paused repayment and froze interest for more than 43 million federal student loan borrowers in response to the COVID-19 pandemic. Since then, the repayment pause has been extended several times, and millions of federal student loan borrowers not having made a single payment in 36 months, including as many as six million borrowers[1] who have never been in active repayment since graduating or stopped out during the pause.

After more than a year of public debate about whether the Administration should forgive all, or a portion of federal student loan debt, in August 2022 the Biden Administration announced plans to provide $10,000 of forgiveness to borrowers who make less than $125,000 a year, $250,000 for couples, and $20,000 for borrowers who received a Pell Grant. If implemented, the Biden Administration estimates that this plan will eliminate student loan debt for as many as 20 million borrowers.[2] Soon after the plan was announced, legal questions were raised that are now in front of the Supreme Court regarding whether the Administration has authority to enact this policy. The Supreme Court is expected to make a final ruling sometime this summer.

In response, the Biden Administration once again extended the student loan pause, calling it the final extension, with an end date 60 days after a Supreme Court ruling, or 60 days after June 30, 2023 – whichever comes first. Regardless of how the Supreme Court rules, at least 20 million borrowers will have remaining student loan balances that they will need to begin paying back to avoid default. Barring further extensions, we’re in the final six months of a three-year federal student loan pause and it is imperative that borrowers start preparing for repayment now.

There have been some attempts to determine how borrowers will struggle to make payments at the end of the repayment pause. One study from the California Policy Lab, estimates nearly 8 million borrowers are at a high risk of missing payments based on other financial well-being indicators, such as past defaults, subprime credit score, and bankruptcy.[3] While this metric alone is discouraging, when compounded with the unprecedented nature of a multi-year pause on repayment, it’s even clearer that student loan borrowers’ financial well-being is in serious jeopardy at the end of this pause. These default risks are compounded by the fact that many borrowers are now facing the harsh realities of inflation. One federal study finds that low-income families are struggling to pay for basic necessities, such as food and housing,[4] with the greatest impact on people of color and those with disabilities who are historically the most likely to default.[5]

The good news is that federal student loan borrowers have options. Before loans go into repayment, borrowers can enroll in a repayment plan that makes the most sense for them financially. Many borrowers can enroll in an income-driven repayment plan where loan payments are capped at 10 percent, or 15 percent of their income. Under these plans, borrowers with adjusted gross incomes less than 150% of the poverty line have a monthly payment of zero. Additionally, borrowers who work for a non-profit or government employer may be eligible for Public Service Loan Forgiveness (PSLF). In cases where borrowers had been in default prior to the pause, the Biden Administration launched Fresh Start to fully rehabilitate their loans and help them enroll in a more affordable repayment plan. With these options at hand, the repayment pause is a unique opportunity to get borrowers enrolled in repayment plans that make the most sense for them and avoid default now and in the future. But we’re at risk of letting this opportunity pass us by.

Since federal student loans were first scheduled to go back into repayment, there have been efforts by policymakers and other stakeholders to get the Department of Education to make a comprehensive plan to help borrowers avoid default going forward.[6] With millions of borrowers expected to go into repayment at once – many of whom have new loan servicers they have never interacted with – and with fewer student loan servicers operating than before the pandemic, strategic communication and outreach is essential.[7] But unfortunately, little effort has been made to engage borrowers and the path to repayment has become increasingly murky. To add to the confusion, student loan servicers have been asked by the U.S. Department of Education to not contact borrowers directly about repayment until it is clear when the pause will end.

Institutions should also take an active role during this period. This is important for the success their students and graduates, as well as their own accountability, where institutions are measured by their graduates’ ability to pay their student loans.

An Institutional Case Study: Southern New Hampshire University (SNHU)

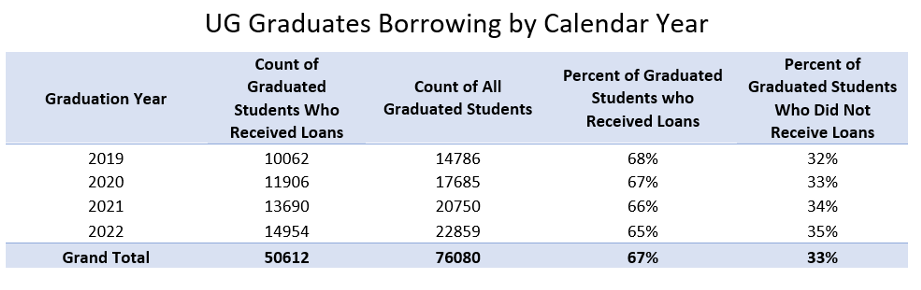

Well before the pandemic, SNHU has been laser focused on affordability and access. In 2021, SNHU marked a decade of frozen tuition for its online programs.[8] Alongside cost stability, SNHU is committed to high-touch financial advising. Part of this is working with students to determine how much they need to borrow to cover their expenses. In doing this, the number of students graduating with no student loan debt has increased year over year. In 2022, 35% of graduates had no student loan debt.

With this foundation of financial responsibility at the center of their mission, SNHU’s financial aid office jumped into action to support alumni borrowers during the payment pause. SNHU hired a dedicated team and stood up a call center to proactively reach out to students, graduates, and alumni about their student loan options. Through this center, borrowers are contacted to talk through their repayment options, and when appropriate, given hands-on support to set up an online account with a student loan servicer and enroll in a payment plan that makes the most sense for them. In many cases, SNHU helps borrowers enroll in income driven repayment plans where they will not be required to make a payment until the repayment pause is over.

This work has been even more essential amidst reports of student loan servicer backlogs and long periods of call waiting. Student loan borrowers most at risk of default often don’t have time to engage with a new servicer, spend hours on call waiting, and navigate a confusing web of repayment options. Some of these borrowers will default not because they don’t have options, but because the system didn’t catch them in time to enroll in an affordable repayment option – this is unacceptable.

The Department of Education, student loan servicers, and institutions should use this period before loans go into repayment to prepare student loan borrowers for what’s next and fervently help them avoid defaulting on their student debt.

Policy Considerations

- The Department of Education should draft and execute an action plan to smoothly end the student loan pause by keeping students out of default – including working with student loan servicers to conduct appropriate outreach to borrowers starting as soon as possible.

- Servicers should prioritize outreach to new student loan borrowers, borrowers who have previously defaulted, and borrowers who were moved from another servicer during the pause. Outreach should prioritize getting borrowers enrolled in the best repayment plan to avoid default.

- Higher education institutions should proactively reach out to recent graduates, and students who have stopped out to help them enroll in income driven repayment plans to avoid default when the pause ends later this year.

Footnotes

[1] Source: FSA Portfolio by loan status, in grace Q3:2020-Q4:2022

[7] The number of major servicers has reduced from eight to six. 9 million borrowers may enter repayment all at once. (Source: FSA Portfolio by loan status, Q4: 2022 in grace and forbearance.)